1. credit 데이터셋

import numpy as np

import pandas as pd

import seaborn as sns

import matplotlib.pyplot as pltcredit_df = pd.read_csv('/content/drive/MyDrive/KDT/머신러닝과 딥러닝/data/credit.csv')

pd.set_option('display.max_columns', 50)

credit_df.head()

# 필요 없는 컬럼 삭제

credit_df.drop(['ID', 'Customer_ID','Name', 'SSN'], axis=1, inplace=True)

credit_df.info()

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 12500 entries, 0 to 12499

Data columns (total 20 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 Age 12500 non-null object

1 Occupation 12500 non-null object

2 Annual_Income 12500 non-null object

3 Num_Bank_Accounts 12500 non-null int64

4 Num_Credit_Card 12500 non-null int64

5 Interest_Rate 12500 non-null int64

6 Num_of_Loan 12500 non-null object

7 Type_of_Loan 11074 non-null object

8 Delay_from_due_date 12500 non-null int64

9 Num_of_Delayed_Payment 11657 non-null object

10 Num_Credit_Inquiries 12264 non-null float64

11 Outstanding_Debt 12500 non-null object

12 Credit_Utilization_Ratio 12500 non-null float64

13 Credit_History_Age 11387 non-null object

14 Payment_of_Min_Amount 12500 non-null object

15 Total_EMI_per_month 12500 non-null float64

16 Amount_invested_monthly 11935 non-null object

17 Payment_Behaviour 12500 non-null object

18 Monthly_Balance 12366 non-null float64

19 Credit_Score 12500 non-null object

dtypes: float64(4), int64(4), object(12)

memory usage: 1.9+ MB# 다중 클래스 분류

credit_df['Credit_Score'].value_counts()

Standard 6943

Poor 3582

Good 1975

Name: Credit_Score, dtype: int64

# object > int로 바꾸기

credit_df['Credit_Score'] = credit_df['Credit_Score'].replace({'Poor': 0, 'Standard': 1, 'Good': 2})credit_df.describe()

sns.barplot(x='Payment_of_Min_Amount', y='Credit_Score', data=credit_df)

plt.figure(figsize= (20, 5))

sns.barplot(x='Occupation', y='Credit_Score', data=credit_df)

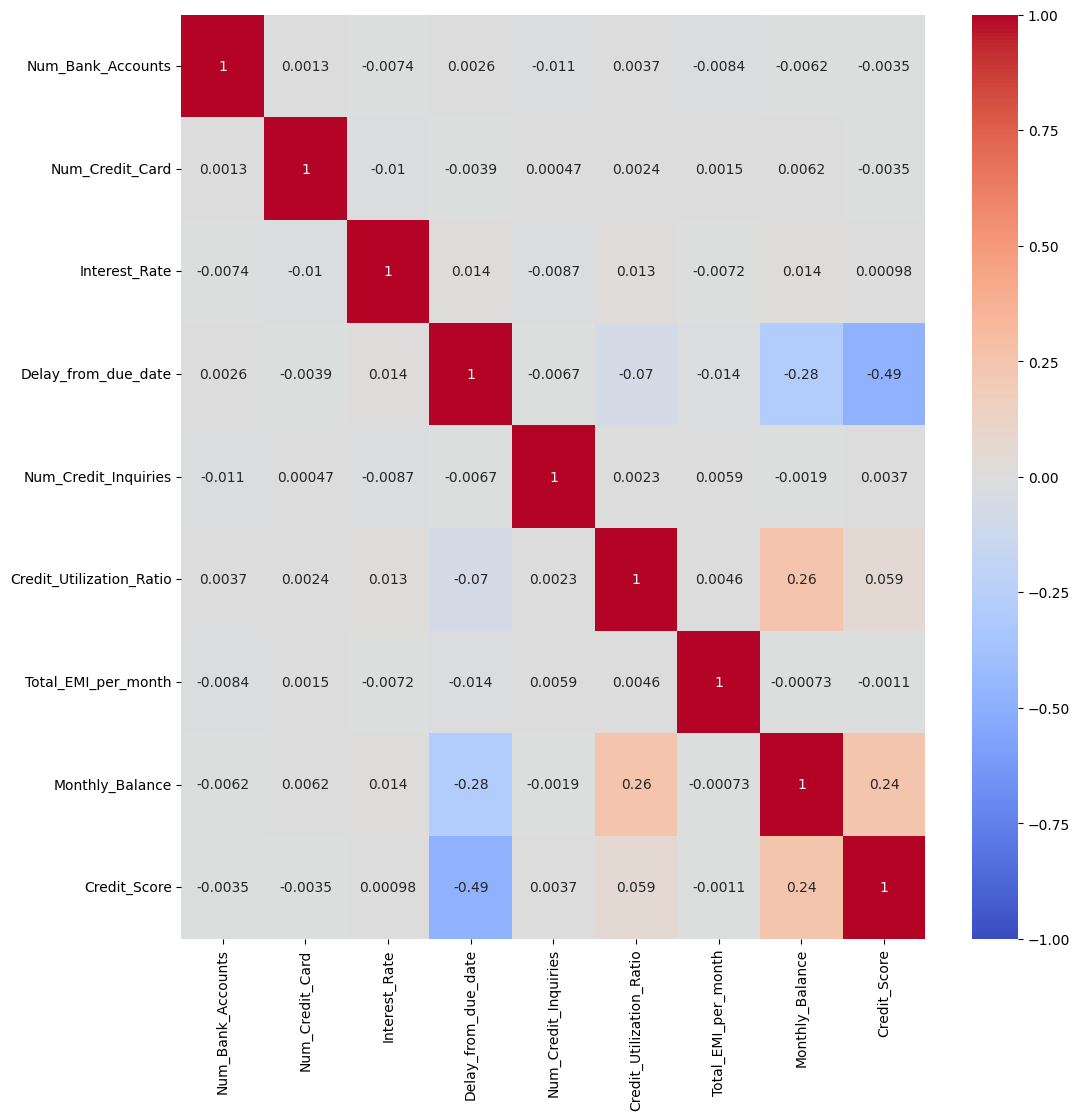

# 컬럼 관련성 보기

plt.figure(figsize=(12,12))

sns.heatmap(credit_df.corr(),cmap='coolwarm', vmin= -1, vmax=1, annot=True)

# object 타입 컬럼 보기

for i in credit_df.columns:

if credit_df[i].dtype == 'O':

print(i)

Age

Occupation

Annual_Income

Num_of_Loan

Type_of_Loan

Num_of_Delayed_Payment

Outstanding_Debt

Credit_History_Age

Payment_of_Min_Amount

Amount_invested_monthly

Payment_Behaviour- 이상치 처리하기

# int 형식이지만 중간에 특수문자'_'가 들어가서 object타입인 컬럼들 고치기

for i in ['Age','Annual_Income', 'Num_of_Loan', 'Num_of_Delayed_Payment', 'Outstanding_Debt', 'Amount_invested_monthly']:

credit_df[i] = pd.to_numeric(credit_df[i].str.replace('_',""))credit_df.info()

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 12500 entries, 0 to 12499

Data columns (total 20 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 Age 12500 non-null int64

1 Occupation 12500 non-null object

2 Annual_Income 12500 non-null float64

3 Num_Bank_Accounts 12500 non-null int64

4 Num_Credit_Card 12500 non-null int64

5 Interest_Rate 12500 non-null int64

6 Num_of_Loan 12500 non-null int64

7 Type_of_Loan 11074 non-null object

8 Delay_from_due_date 12500 non-null int64

9 Num_of_Delayed_Payment 11657 non-null float64

10 Num_Credit_Inquiries 12264 non-null float64

11 Outstanding_Debt 12500 non-null float64

12 Credit_Utilization_Ratio 12500 non-null float64

13 Credit_History_Age 11387 non-null object

14 Payment_of_Min_Amount 12500 non-null object

15 Total_EMI_per_month 12500 non-null float64

16 Amount_invested_monthly 11935 non-null float64

17 Payment_Behaviour 12500 non-null object

18 Monthly_Balance 12366 non-null float64

19 Credit_Score 12500 non-null int64

dtypes: float64(8), int64(7), object(5)

memory usage: 1.9+ MB# Credit_History_Age의 데이터를 개월로 변경

예) 22 Years and 1 Months -> 22 * 12 + 1

credit_df['Credit_History_Age'] = credit_df['Credit_History_Age'].str.replace(' Months','')

credit_df['Credit_History_Age'] =

pd.to_numeric(credit_df['Credit_History_Age'].str.split(' Years and ',expand = True)[0])*12

+ pd.to_numeric(credit_df['Credit_History_Age'].str.split(' Years and ',expand = True)[1])# 다른 방법

credit_df['New_Credit_History_Age'] = credit_df['Credit_History_Age'].apply(lambda x: int(x.split(' ')[0]) * 12 + int(x.split(' ')[-2]) if pd.notna(x) else 0)

credit_df['New_Credit_History_Age']credit_df.describe()

credit_df[credit_df['Age'] < 0]

// 115 rows × 20 columns

credit_df = credit_df[credit_df['Age'] >= 0]credit_df.sort_values('Age').tail(20)

sns.boxplot(y=credit_df['Age'])

credit_df[credit_df['Age']>= 100].sort_values('Age')

// 260 rows × 20 columns

# 100살이 넘는 사람 데이터가 260개

# 110살 넘지 않는 데이터로만 다시 저장

credit_df = credit_df[credit_df['Age'] < 110]

✔️ 은행계좌가 10개 이상인 사람의 비율 확인

len(credit_df[credit_df['Num_Bank_Accounts'] > 10]) / len(credit_df)

// 0.013029853207982847credit_df = credit_df[credit_df['Num_Bank_Accounts'] <= 10]len(credit_df[credit_df['Num_Credit_Card'] > 20]) / len(credit_df)

// 0.021975267379679145

credit_df = credit_df[credit_df['Num_Credit_Card'] <= 20]credit_df = credit_df[credit_df['Interest_Rate'] <= 40]

credit_df = credit_df[(credit_df['Num_of_Loan'] <= 10) & (credit_df['Num_of_Loan'] >= 0)]

credit_df = credit_df[credit_df['Delay_from_due_date'] >= 0]len(credit_df[credit_df['Num_of_Delayed_Payment'] > 30])

// 80

credit_df = credit_df[(credit_df['Num_of_Delayed_Payment'] <= 30) & (credit_df['Num_of_Delayed_Payment'] >= 0)]credit_df.info()

<class 'pandas.core.frame.DataFrame'>

Int64Index: 10004 entries, 0 to 12498

Data columns (total 20 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 Age 10004 non-null int64

1 Occupation 10004 non-null object

2 Annual_Income 10004 non-null float64

3 Num_Bank_Accounts 10004 non-null int64

4 Num_Credit_Card 10004 non-null int64

5 Interest_Rate 10004 non-null int64

6 Num_of_Loan 10004 non-null int64

7 Type_of_Loan 8893 non-null object

8 Delay_from_due_date 10004 non-null int64

9 Num_of_Delayed_Payment 10004 non-null float64

10 Num_Credit_Inquiries 9816 non-null float64

11 Outstanding_Debt 10004 non-null float64

12 Credit_Utilization_Ratio 10004 non-null float64

13 Credit_History_Age 9106 non-null float64

14 Payment_of_Min_Amount 10004 non-null object

15 Total_EMI_per_month 10004 non-null float64

16 Amount_invested_monthly 9549 non-null float64

17 Payment_Behaviour 10004 non-null object

18 Monthly_Balance 9895 non-null float64

19 Credit_Score 10004 non-null int64

dtypes: float64(9), int64(7), object(4)

memory usage: 1.6+ MB- 결측치 확인

credit_df['Num_Credit_Inquiries'] = credit_df['Num_Credit_Inquiries'].fillna(0)credit_df.isna().mean()

Age 0.000000

Occupation 0.000000

Annual_Income 0.000000

Num_Bank_Accounts 0.000000

Num_Credit_Card 0.000000

Interest_Rate 0.000000

Num_of_Loan 0.000000

Type_of_Loan 0.111056

Delay_from_due_date 0.000000

Num_of_Delayed_Payment 0.000000

Num_Credit_Inquiries 0.000000

Outstanding_Debt 0.000000

Credit_Utilization_Ratio 0.000000

Credit_History_Age 0.089764

Payment_of_Min_Amount 0.000000

Total_EMI_per_month 0.000000

Amount_invested_monthly 0.045482

Payment_Behaviour 0.000000

Monthly_Balance 0.010896

Credit_Score 0.000000

dtype: float64sns.displot(credit_df['Credit_History_Age'])

sns.displot(credit_df['Amount_invested_monthly'])

sns.displot(credit_df['Monthly_Balance'])

# 한쪽으로 치우쳐진 데이터가 많기때문에 평균이 아닌 중앙값으로 결측치 대체

credit_df= credit_df.fillna(credit_df.median())credit_df.isna().mean()

Age 0.000000

Occupation 0.000000

Annual_Income 0.000000

Num_Bank_Accounts 0.000000

Num_Credit_Card 0.000000

Interest_Rate 0.000000

Num_of_Loan 0.000000

Type_of_Loan 0.111056

Delay_from_due_date 0.000000

Num_of_Delayed_Payment 0.000000

Num_Credit_Inquiries 0.000000

Outstanding_Debt 0.000000

Credit_Utilization_Ratio 0.000000

Credit_History_Age 0.000000

Payment_of_Min_Amount 0.000000

Total_EMI_per_month 0.000000

Amount_invested_monthly 0.000000

Payment_Behaviour 0.000000

Monthly_Balance 0.000000

Credit_Score 0.000000

dtype: float64

# 문제.

# type_of_Loan의 모든 대출 상품을 변수에 저장

# 각 대출 상품에 대한 이름으로 컬럼을 만들고 대출 상품이 있는 경우 해당 컬럼에 1을 저장(원 핫 인코딩 방식)

credit_df['Type_of_Loan'] = credit_df['Type_of_Loan'].str.replace('and ', '')

credit_df['Type_of_Loan'] = credit_df['Type_of_Loan'].fillna('No Loan')

type_list = set(credit_df['Type_of_Loan'].str.split(', ').sum())

type_list

{'Auto Loan',

'Credit-Builder Loan',

'Debt Consolidation Loan',

'Home Equity Loan',

'Mortgage Loan',

'No Loan',

'Not Specified',

'Payday Loan',

'Personal Loan',

'Student Loan'}for i in type_list:

credit_df[i]= credit_df['Type_of_Loan'].apply(lambda x: 1 if i in x else 0)

credit_df.drop('Type_of_Loan', axis=1, inplace=True)

credit_df.info()

<class 'pandas.core.frame.DataFrame'>

Int64Index: 10004 entries, 0 to 12498

Data columns (total 29 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 Age 10004 non-null int64

1 Occupation 10004 non-null object

2 Annual_Income 10004 non-null float64

3 Num_Bank_Accounts 10004 non-null int64

4 Num_Credit_Card 10004 non-null int64

5 Interest_Rate 10004 non-null int64

6 Num_of_Loan 10004 non-null int64

7 Delay_from_due_date 10004 non-null int64

8 Num_of_Delayed_Payment 10004 non-null float64

9 Num_Credit_Inquiries 10004 non-null float64

10 Outstanding_Debt 10004 non-null float64

11 Credit_Utilization_Ratio 10004 non-null float64

12 Credit_History_Age 10004 non-null float64

13 Payment_of_Min_Amount 10004 non-null object

14 Total_EMI_per_month 10004 non-null float64

15 Amount_invested_monthly 10004 non-null float64

16 Payment_Behaviour 10004 non-null object

17 Monthly_Balance 10004 non-null float64

18 Credit_Score 10004 non-null int64

19 No Loan 10004 non-null int64

20 Auto Loan 10004 non-null int64

21 Debt Consolidation Loan 10004 non-null int64

22 Mortgage Loan 10004 non-null int64

23 Not Specified 10004 non-null int64

24 Home Equity Loan 10004 non-null int64

25 Personal Loan 10004 non-null int64

26 Student Loan 10004 non-null int64

27 Credit-Builder Loan 10004 non-null int64

28 Payday Loan 10004 non-null int64

dtypes: float64(9), int64(17), object(3)

memory usage: 2.3+ MBcredit_df['Occupation'].value_counts()

_______ 674

Lawyer 664

Mechanic 646

Scientist 640

Engineer 640

Architect 633

Teacher 624

Developer 621

Entrepreneur 620

Media_Manager 616

Accountant 611

Doctor 608

Musician 607

Journalist 606

Manager 602

Writer 592

Name: Occupation, dtype: int64# 어차피 모델은 카테고리로 인식하기때문에 꼭 바꿔줘야하는건 아니지만, 보기 편하게 변경 진행

credit_df['Occupation'] = credit_df['Occupation'].replace('_______', 'Unknown')

credit_df['Occupation'].value_counts()

Unknown 674

Lawyer 664

Mechanic 646

Scientist 640

Engineer 640

Architect 633

Teacher 624

Developer 621

Entrepreneur 620

Media_Manager 616

Accountant 611

Doctor 608

Musician 607

Journalist 606

Manager 602

Writer 592

Name: Occupation, dtype: int64credit_df['Payment_Behaviour'].value_counts()

Low_spent_Small_value_payments 2506

High_spent_Medium_value_payments 1794

High_spent_Large_value_payments 1453

Low_spent_Medium_value_payments 1376

High_spent_Small_value_payments 1136

Low_spent_Large_value_payments 995

!@9#%8 744 # 알 수 없는 값이 있음

Name: Payment_Behaviour, dtype: int64credit_df['Payment_Behaviour'] = credit_df['Payment_Behaviour'].str.replace('!@9#%8','Unknown')

credit_df['Payment_Behaviour'].value_counts()

Low_spent_Small_value_payments 2506

High_spent_Medium_value_payments 1794

High_spent_Large_value_payments 1453

Low_spent_Medium_value_payments 1376

High_spent_Small_value_payments 1136

Low_spent_Large_value_payments 995

Unknown 744

Name: Payment_Behaviour, dtype: int64credit_df = pd.get_dummies(credit_df, columns = {'Payment_Behaviour','Occupation','Payment_of_Min_Amount'})2. lightGBM(LGBM)

Microsoft에서 개발한 LightGBM은 리프 중심 히스토그램 기반의 Gradient Boosting Framework로, 효율적이고 빠른 학습을 제공합니다. GBM은 모델 간의 앙상블을 통해 예측 정확도를 향상시키는 부스팅 알고리즘입니다. LightGBM은 이를 모델1을 통해 y를 예측하고, 모델2, 모델3에 차례로 데이터를 넣어 y를 예측하는 방식으로 구현합니다.

앙상블 모델

앙상블은 여러 개별 모델을 결합하여 하나의 강력한 모델을 형성하는 기술입니다. 이는 각 모델의 약점을 서로 보완하고 강점을 결합하여 높은 정확도와 안정성을 달성하는 데 도움이 됩니다. 1

junyealim.tistory.com

- LightGBM은 대용량 데이터셋에서 다른 Gradient Boosting 알고리즘보다 빠르게 학습됩니다. 특히 작은 데이터셋에서도 높은 성능을 보여줍니다.

- 메모리 사용량이 비교적 적어 대용량 데이터셋을 다룰 때에도 효율적으로 동작합니다.

- 과적합을 방지하기 위해 LightGBM은 조기 중단을 지원합니다. 이를 통해 모델의 학습을 일찍 멈출 수 있어, 불필요한 계산을 줄일 수 있습니다.

LightGBM은 작은 데이터셋에서 과적합 가능성이 높습니다. 일반적으로 10,000개 이상의 데이터셋을 사용하는 것이 권장됩니다.

from sklearn.model_selection import train_test_split

X_train, X_test, y_train, y_test = train_test_split(credit_df.drop('Credit_Score', axis=1),credit_df['Credit_Score'], test_size= 0.2, random_state=2023)

X_train.shape, y_train.shape // ((8003, 51), (8003,))

X_test.shape, y_test.shape // ((2001, 51), (2001,))from lightgbm import LGBMClassifier

base_model = LGBMClassifier(random_state=2023)

base_model.fit(X_train,y_train)

pred = base_model.predict(X_test)from sklearn.metrics import accuracy_score, confusion_matrix, classification_report, roc_auc_scoreaccuracy_score(y_test, pred)

// 0.7251374312843578

confusion_matrix(y_test,pred)

//array([[409, 144, 25],

[154, 855, 108],

[ 4, 115, 187]])

print(classification_report(y_test, pred))

precision recall f1-score support

0 0.72 0.71 0.71 578

1 0.77 0.77 0.77 1117

2 0.58 0.61 0.60 306

accuracy 0.73 2001

macro avg 0.69 0.69 0.69 2001

weighted avg 0.73 0.73 0.73 2001

proba = base_model.predict_proba(X_test)

array([[1.85999520e-01, 5.12892812e-01, 3.01107668e-01],

[3.00755505e-02, 9.69418975e-01, 5.05474881e-04],

[1.77775175e-01, 4.70635184e-01, 3.51589641e-01],

...,

[6.05786945e-02, 6.17182265e-01, 3.22239040e-01],

[2.39508935e-01, 7.60120500e-01, 3.70565507e-04],

[2.00383699e-02, 9.79857031e-01, 1.04599097e-04]])

# 1.85999520e-01, 5.12892812e-01, 3.01107668e-01

# (0.18599952, 0.512892812, 0.301107668)roc_auc_score(y_test,proba, multi_class='ovr')

// 0.8932634160489487# 다중 클래스 분류여서 multi_class 항목을 선택해주어야한다! 대부분 OvR 전략 사용

- OvR(One-vs-Rest): 각 클래스마다 하나의 이진 분류기를 생성하고, 해당 클래스를 기준으로 그 클래스와 나머지 모든 클래스를 구분하는 이진 분류를 수행합니다. 가장 높은 확률을 가진 클래스를 선택합니다.

- OvO(One-vs-One): 클래스의 개수가 N이면 N(N-1)/2개의 이진 분류기를 만들어 각각 두 클래스를 구분합니다. 입력 데이터를 각 이진 분류기에 통과시켜 가장 많이 선택된 클래스를 최종 클래스로 선택합니다.

✔️리프 중심 히스토그램 기반 알고리즘

트리를 균형적으로 분할하는 것이 아니라, 최대한 불균형하게 분할하는 부스팅 프로그램의 성격

특성들의 분포를 히스토그램으로 나타내고, 해당 히스토그램을 이용하여 빠르게 후보 분할 기준을 선택

후보 분할 기준 중에서 최적의 분할 기준을 선택하기 위해, 데이터 포인트들을 히스토그램에 올바르게 배치하고, 이용하여 최적의 분할 기준을 선택함

앙상블 모델

앙상블은 여러 개별 모델을 결합하여 하나의 강력한 모델을 형성하는 기술입니다. 이는 각 모델의 약점을 서로 보완하고 강점을 결합하여 높은 정확도와 안정성을 달성하는 데 도움이 됩니다. 1

junyealim.tistory.com

3-1. 그래디언트 부스팅에 lightGBM 참고